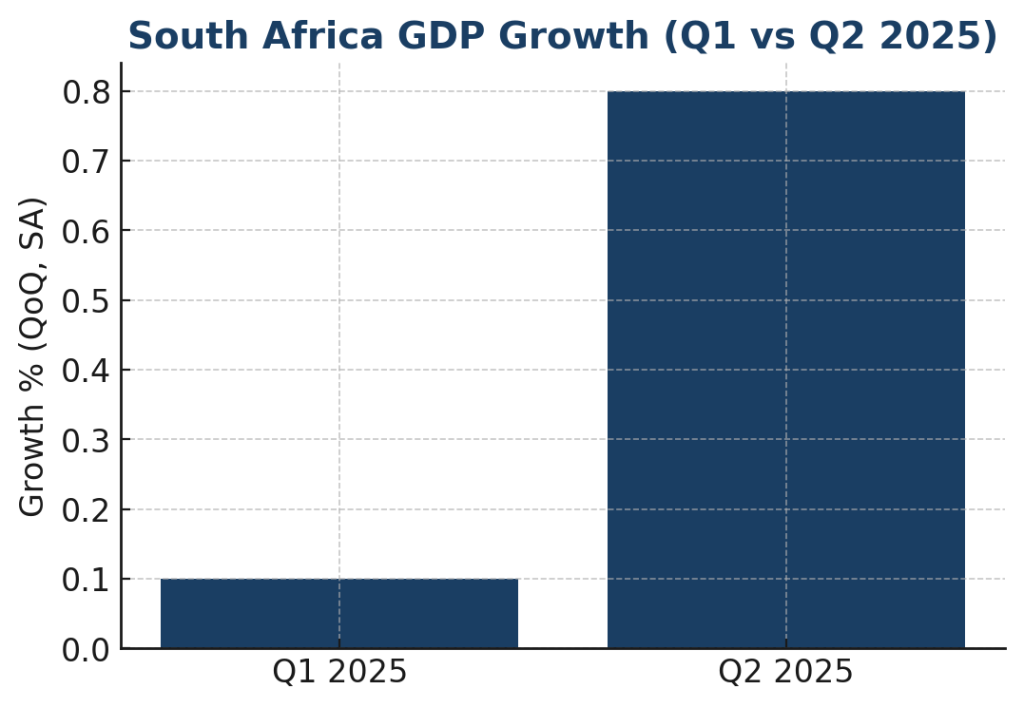

South Africa’s economy showed renewed momentum in the second quarter of 2025, with gross domestic product (GDP) rising 0.8% on a seasonally adjusted basis. This marks a stronger rebound compared to the modest 0.1% growth recorded in the first quarter, signaling that key industries are finding traction despite ongoing structural challenges.

Key Drivers of Growth

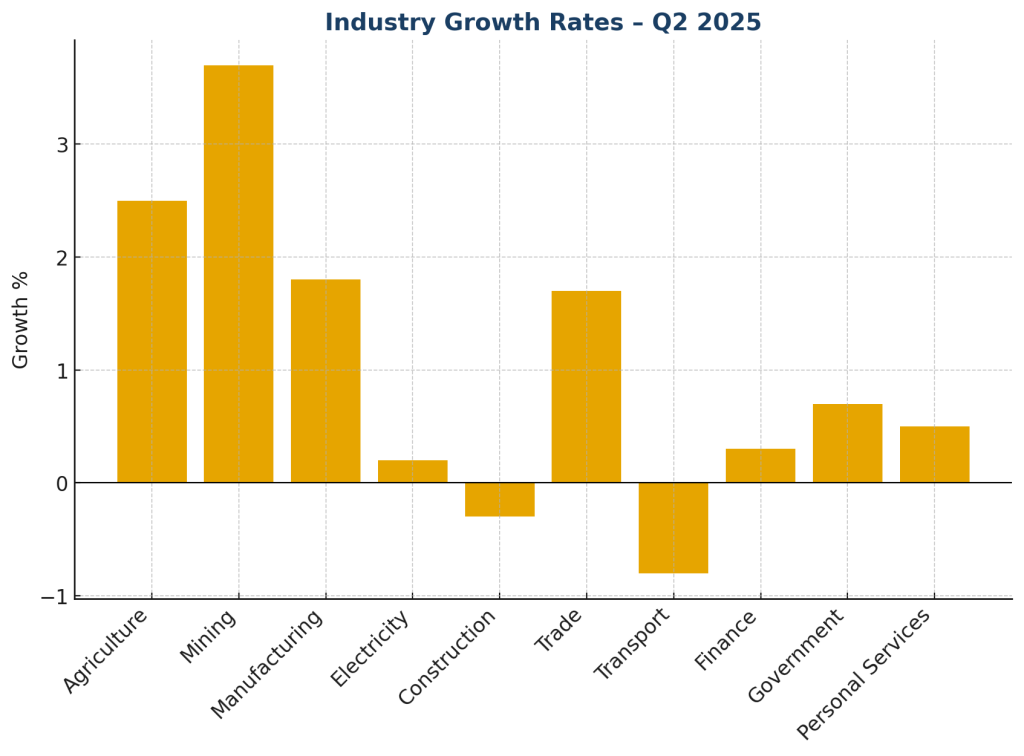

The manufacturing sector led the charge, growing by 1.8% and contributing significantly to national output. The expansion was broad-based, with strength in petroleum, chemicals, plastics, and motor vehicles. Similarly, the mining industry delivered a robust 3.7% increase, supported by platinum group metals, gold, and chromium ore production. Retail trade, catering, and accommodation also added momentum with 1.7% growth, reflecting a pick-up in household spending and tourism-related activities.

On the other hand, the transport, storage, and communication industry contracted by 0.8%, making it the largest drag on GDP this quarter. The construction sector also slipped slightly, weighed down by weak performance in residential and non-residential building projects.

Spending Patterns: Households Driving Demand

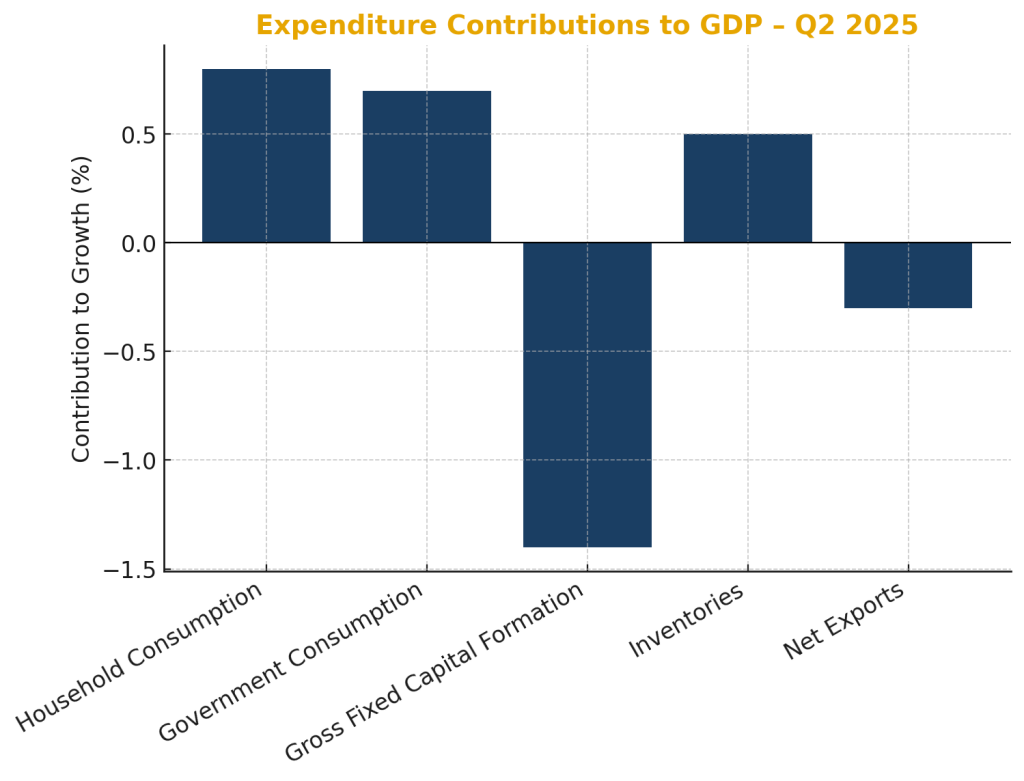

On the expenditure side, GDP rose 0.7%. Household consumption increased by 0.8%, accounting for most of the expansion. Consumers spent more on restaurants, hotels, clothing, footwear, and transport, suggesting confidence is slowly returning in certain spending categories. Government expenditure also edged higher (+0.7%), reflecting increased employment in public services.

However, investment activity remained under pressure, with gross fixed capital formation declining by 1.4%. Weakness in transport equipment and non-residential construction continues to hold back growth prospects. Encouragingly, inventory build-ups across mining, manufacturing, and logistics provided a temporary buffer.

When it comes to spending, households took center stage, almost as if South Africa now has a Ministry of Enjoyment with money flowing into restaurants, hotels, clothing, and entertainment. People are clearly choosing lifestyle over long-term planning.

But here’s the catch, while we’re quick to spend at the mall or on a weekend away, financial services and investments only grew 0.3%. This gap highlights a serious shortfall in financial education. Many households are consuming but not building wealth.

Trade Headwinds Persist

International trade was a net drag on growth. Exports contracted by 3.2%, particularly in metals, vegetable products, and vehicle exports, while imports dropped 2.1%, linked to lower demand for chemicals, machinery, and minerals. This highlights persistent vulnerabilities in South Africa’s trade balance.

What This Means for Businesses and Investors

For businesses, the latest GDP data reflects a mixed but cautiously optimistic environment. Domestic consumption is strengthening, offering opportunities in retail, hospitality, and consumer services. At the same time, weak investment and trade constraints underscore the need for prudent planning, diversification, and resilience strategies.

At ISEN Business Advisory, we believe that clients, whether individuals or SMEs should remain alert to sectoral shifts. Manufacturing, mining, and consumer-facing industries are showing growth momentum, while construction and transport remain under strain. Strategic positioning, tax-efficient planning, and proactive financial management will be key to navigating this evolving economic landscape.

ISEN Business Advisory regularly assists individuals and SMEs in navigating their tax and financial strategies. For guidance or assistance with, contact us at admin@isenadvisory.co.za.